IRS Form 720 Updated for 2025 PCORI Fee Filings

On Friday, June 26, the IRS updated its Form 720 to reflect the PCORI fee amounts and plan year end dates applicable to plan years ending in the 2025 calendar year. Because the amount on column (b) on Line 133(c) now correctly lists $3.47 and Line 133(d) now correctly lists $3.84 (and no longer list $3.22 and $3.47, respectively), employers and other plan sponsors are now able to complete and submit their Form 720 for PCORI fees ending in 2025 (when applicable).

- Self-funded medical plans ending in 2025, including level-funded plans, HRAs, ICHRAs, QSEHRAs, MERPs, and other less common arrangements as described on the IRS chart found at: https://www.irs.gov/newsroom/application-of-the-patient-centered-outcomes-research-trust-fund-fee-to-common-types-of-health-coverage-or-arrangements.

- Exceptions: Fully insured plans are the carrier’s responsibility, and excepted benefits are exempt, including stand-alone vision or dental plans, HSAs, and health FSAs that qualify as an excepted benefit.

As background, the ACA requires certain group health plans to pay a Patient-Centered Outcomes Research Institute (PCORI) fee. PCORI fees are automatically included in the premiums and submitted by the insurer for fully insured plans, however employers and other plan sponsors must calculate and remit this fee to the IRS themselves for any level funded and self-insured (self-funded) health plans, including HRAs, ICHRAs, QSEHRAs, and most MERPs.

Although the fee is incurred on a per plan year basis, the fee itself is remitted on an annual basis using the second quarter IRS Form 720. PCORI fees must be remitted to the IRS by July 31 of the calendar year following the calendar year in which the plan year ended (or the next business day if July 31 lands on a weekend). For example, the fees applicable to plan years ending any time during the 2025 calendar year are due to the IRS by Jul. 31, 2026.

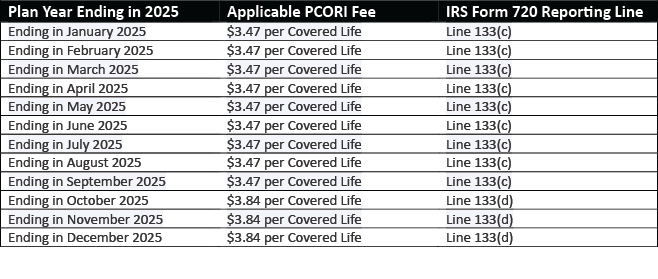

The rate at which plans are taxed is different for plan years ending in January through September compared to those ending in October through December. Specifically for plan years ending in the 2025 calendar year, the PCORI fees due in 2026 use the following rates:

- $3.47 per covered life for plan years ending prior to October 1, 2025. This fee is reported on Form 720, Line 133(c).

- $3.84 per covered life for plan years ending on or after October 1, 2025. This fee is reported on Form 720, Line 133(d).

Broken down by plan year end date, the full list is as follows:

For self-insured health plans, including level funded health plans, covered lives’ include not only primary insureds such as employees and former employees enrolled on the plan, but also the secondary insureds such as spouses and dependents. For HRAs (including ICHRAs, QSEHRAs, and MERPs), only the primary insureds such as the employees and former employees are counted, while secondary insureds are disregarded.

More information about the special rule for employers sponsoring multiple self-insured plans, calculating PCORI fees for a short plan year, reporting multiple PCORI fees both ending in the same calendar year can be found in our supplemental resource entitled “PCORI Fee Basics.” More information about the four prescribed methods to calculate PCORI fees can be found in our “PCORI Fee Calculation Methods.”

Failing to correctly calculate and report PCORI fees may result in the following IRS penalties and interest:

- The potential penalty for failure to file is 5% of the unpaid PCORI fee per month, up to a maximum of 25% of the original tax owed (achieved after the 5th month late).

- The penalty for failure to pay is 0.5% of the unpaid PCORI fee per month, up to a maximum of 25%.

- When applicable, there is a minimum penalty of the lesser of $100 or 100% of the tax owed, however it appears this minimum is not always enforced.

- Interest on the late payments and unpaid penalties accrues daily using rates adjusted quarterly.

While a lower PCORI fee generally means a relatively low penalty, the interest in particular can slowly build up over time. Even when initial calculations are provided by the TPA or your benefits advisory team, plan sponsors are ultimately responsible for the accuracy of their tax filings. It is essential to confirm the enrollment counts and math, and to consult with your tax advisors when necessary.

1. Confirm Applicability

- Identify whether the plan qualifies as self-funded or is a fully insured plan with an HRA or ICHRA for a plan year that ended in 2025 (when calculating fees due by July 31st 2026). If a self-funded plan, HRA, or ICHRA was implemented, but does not end until 2026, then its PCORI fee is not due until July 31st 2027.

Determine the plan year end date to set the filing deadline and identify the correct fee ($3.47 or $3.84).

2. Calculate Fees

- Request enrollment reports from vendors for participant counts. For HRAs and ICHRAs, only the number of primary insureds (employees) are needed. For self-funded or level funded group health plans, you need both the primary insureds by tier (self-only vs. all other election tiers) as well as the total number of covered individuals (including spouses and dependents).

- Choose an IRS-approved counting method. Employers can select the method resulting in the lowest cost.

3. File and Pay

- Complete IRS Form 720 in its entirety. Do not use a Form 720 that has not yet been updated to reflect the correct plan year dates and dollar amounts on Line 133. That is, for plan years ending in 2025, column (b) on Line 133(c) must list $3.47 and Line 133(d) must list $3.84 (and not $3.22 and $3.47, respectively).

- In addition to completing the filing organization’s legal name, Federal Employer Identification Number (FEIN) and address, they must also enter the tax filing quarter month and year (i.e., “June 2026” when filing PCORI fees in 2026 for plans ending in 2025).

- On or before July 31, 2025, submit Form 720 and payment electronically or by mail using the Form 720-V payment voucher with the “2nd Quarter” circle filled in.

Retain records if proof of payment or counting method is ever requested by the IRS. We are not aware of any portal to look up past filings, so keeping records for four years is crucial.